S&P500 LDN Open Trading Update 21/5/26

S&P500 LDN Open Trading Update 21/5/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

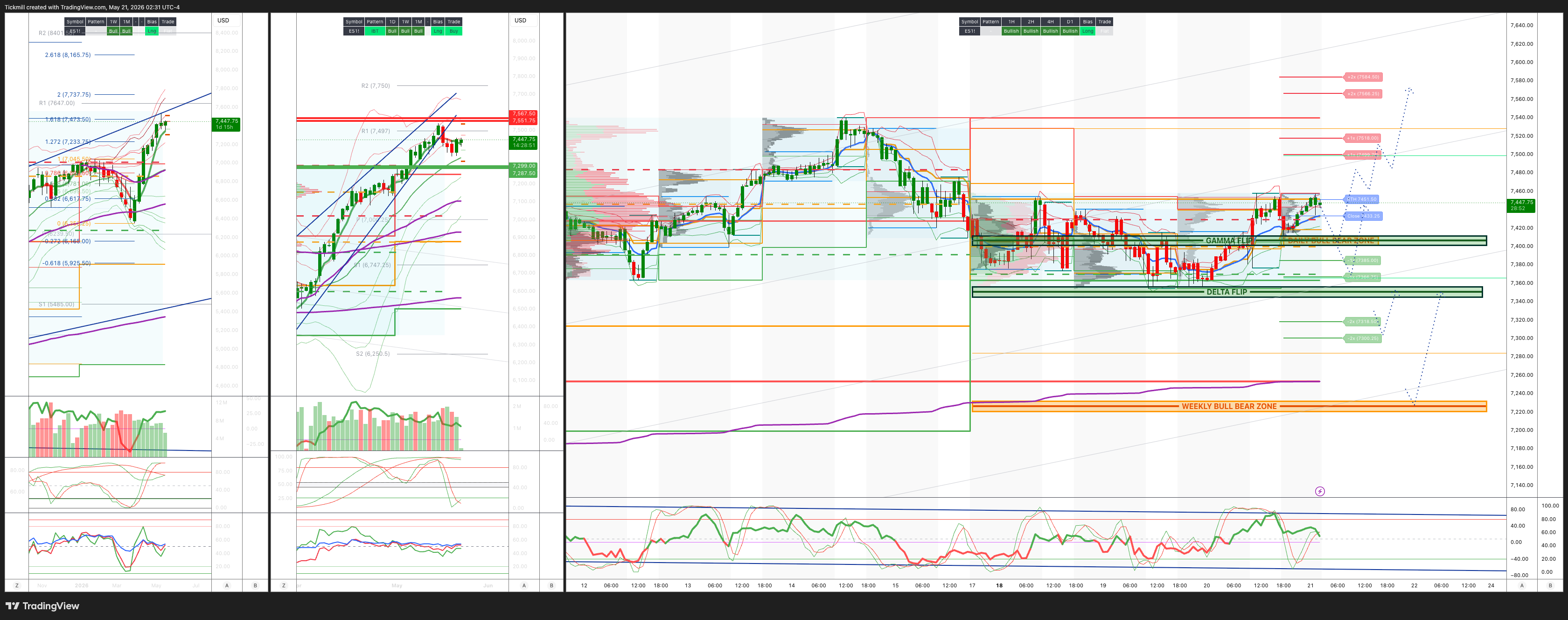

WEEKLY BULL BEAR ZONE 7220/30

WEEKLY RANGE RES 7286 SUP 7550

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.01 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BALANCE 7475/7354

WEEKLY VWAP BULLISH 7292

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFL - 7415

WEEKLY STRUCTURE – OTFH - 7363

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7410/00

GAMMA FLIP 7407

DELTA FLIP 7350

DAILY RANGE RES 7499 SUP 7367

2 SIGMA RES 7566 SUP 7300

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON ACCEPTANCE ABOVE 7460 TARGET DAILY RANGE RES

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Mo’Bounce + Peace Hopes + NVDA’

US equities ripped higher on a cleaner macro tape as peace hopes in the Middle East drove a sharp oil reversal and a rally in rates. The S&P 500 gained 108bps to 7,433 despite a USD 1bn MOC imbalance to sell, the NDX rose 166bps to 29,298, the Russell 2000 surged 256bps to 2,817, and the Dow added 131bps to close above 50,000 at 50,009. Volumes were a little below trend at 18.65bn shares versus a YTD daily average of 19bn. Cross-asset moves were decisively supportive for risk: WTI fell 542bps to USD 98.52, the US 10-year yield dropped 9bps to 4.57%, VIX declined 343bps to 17.44, gold gained 143bps to USD 4,547, DXY slipped 22bps to 99.11, and Bitcoin rose 81bps to USD 77,584.

The driver was straightforward: the market latched onto reports that Washington and Tehran were putting the “finishing touches” on a draft agreement. With crude down more than 5% and the 10-year yield lower by roughly 8-9bps, the two largest macro constraints on equities eased at the same time. That created the conditions for a broad melt-up, particularly after several sessions of painful momentum unwinds and factor de-risking. The rally was not simply a tech bounce; small caps led, equal-weight improved, and risk appetite broadened as the oil/rates shock faded.

Momentum bounced around 3% in anticipation of NVDA earnings, which helped stabilize the AI complex after the recent drawdown. The move is important because it shows how quickly the market can re-embrace crowded leadership when the macro overhang softens. But single-stock flows were still muted, and the floor was only a 4 out of 10 in activity. Investors were broadly in “wait-and-see” mode, content to sit out some of the factor chop ahead of NVDA and the next batch of consumer earnings. Asset managers finished better to buy, while hedge-fund flows were roughly flat.

NVDA delivered a down-the-fairway print after the close. The quarter was solid, with Q1 revenue of USD 81.5bn versus consensus around USD 79bn, and Q2 guidance of USD 91bn versus consensus around USD 87bn. Capital returns should be well received, with the company raising its buyback authorization by USD 80bn and increasing the dividend to 25 cents per quarter. The stock was flattish after hours, which is consistent with a print that was strong but largely within the range of elevated expectations. The call remains important, especially for commentary on datacenter visibility, Rubin/Blackwell demand, agentic AI, non-hyperscaler customers, ASIC competition, and gross margins.

The positioning setup in NVDA remains heavy but less extreme than before. The desk had it as a 9 out of 10 on positioning. The stock is still well owned across investor types and has rallied roughly 35% from the end-of-March low, but it is no longer the “max long” it once was. Tech specialists have rotated further out the risk curve in search of the next AI trade, while generalists have used NVDA as a source of funds. That distinction matters: the stock can still act as an AI anchor, but it may not produce the same forced upside chase unless the call adds incremental upside to the long-term story.

The key interpretive point on NVDA is that the numbers were good enough to validate the AI capex cycle, but perhaps not enough by themselves to trigger a major re-rating. A beat-and-raise was expected. The stock needs the call to provide additional evidence that the USD 1 trillion datacenter visibility can move higher, that agentic AI expands CPU and rack-level opportunities, that non-hyperscaler demand is broadening, and that mid-70s gross margins are sustainable despite memory and component inflation. If management delivers on those points, the print should be supportive for AI broadly even if the immediate stock reaction is muted.

Tomorrow shifts the focus to the consumer. WMT is the main event, alongside RL and WSM in the morning, then DECK and ROST after the close. All five are expected to beat. For WMT, the quarter is expected to be good, and the key issue is whether management flags any slowdown after TGT sold off around 6% on the 2Q debate. Most feedback suggests WMT will sound great on 1Q and fine on 2Q. The final comp bogey for Walmart US appears to be around +4.5% to +5%, with most expectations realistically closer to +5%. The bear case is mainly valuation rather than the core business.

This consumer setup matters because today’s rally was helped by lower oil and lower yields. If WMT confirms that the consumer is still resilient, the market can broaden further beyond AI and momentum. If WMT hints at slowing lower-income demand, discretionary weakness, or margin pressure, then the rally may remain dependent on mega-cap tech and macro relief rather than genuine earnings breadth.

Derivatives activity showed that investors are still hedging despite the rally. As Momentum reverted into the green, vol-desk flows tilted toward hedging. The most notable trades were three large clips of 100k VIX one-week call spreads bought in the market. The desk also flagged persistent large Jan-2028 downside buyers in software over the course of the week. This is important because it shows that investors are participating in upside but still preparing for renewed volatility or a factor reversal.

The spot/vol relationship remained unusual. Fixed-strike vols went bid alongside spot, producing another episode of spot-up/vol-up behavior. That suggests the market is realizing more to the upside on good news than to the downside on bad news, while conviction in options remains limited. The rest-of-week straddle compressed to around 98bps, reflecting some event decay after the rally and into NVDA, but the demand for VIX call spreads and software downside indicates that investors do not fully trust the move.

The trading takeaway is that the market just received a near-perfect short-term macro relief impulse: oil down sharply, yields lower, VIX lower, and peace headlines improving. That is enough to reverse some of the momentum damage and broaden risk appetite. But the rally still needs confirmation. NVDA’s headline print supports the AI thesis, but the call must provide the incremental long-term confidence investors need. WMT must confirm the consumer is not cracking. And most importantly, the Middle East headlines need to progress from “draft agreement” to durable de-escalation.

For now, the right stance is constructive but not complacent. The macro shock has eased, and if crude remains below USD 100 and the 10-year stabilizes below recent highs, equities can continue to repair. Small caps and equal-weight may have room to catch up if rates keep falling. AI can stabilize if NVDA’s call reinforces datacenter durability. Consumer can broaden the rally if WMT delivers cleanly.

But the hedging flows are telling. Investors are not removing protection; they are adding short-dated VIX upside and long-dated software downside. That argues against chasing the rally indiscriminately. Use the macro relief to rebalance crowded exposures, maintain some downside convexity, and look for broader opportunities in areas that benefit from lower oil and lower yields.Today was a strong risk-on reversal driven by peace hopes, lower oil, and lower rates. NVDA delivered a solid beat-and-raise, but the stock reaction shows the bar was high. The next phase depends on whether the call adds upside to the AI story and whether WMT confirms consumer resilience. If both land well and the oil/rates relief holds, the market can broaden. If not, today’s rally may prove to be another sharp squeeze inside a still-fragile factor tape.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!