Institutional Insights: BofA Six Reasons To Short The Euro

Six Reasons to Short EUR/USD into Summer

The recommendation is to position for euro weakness into summer through a 3-month EUR/USD 1.15/1.13 put spread.

At spot around 1.1610, with vols around 6.22% / 6.72%, the structure costs roughly 0.3591%. The trade expresses a moderate bearish EUR/USD view, targeting a move below 1.15 toward 1.13 over the next three months, while limiting premium outlay.

The main risks are a quick US-Iran deal that reopens the Strait of Hormuz, supportive euro summer seasonality, and softer US data.

## Trade recommendation

Buy EUR/USD 3m 1.15/1.13 put spread

| Spot | 1.1610 |

| Structure | 3m put spread |

| Strikes | 1.15 / 1.13 |

| Indicative vol | 6.22% / 6.72% |

| Premium | 0.3591% |

| Directional view | EUR/USD lower into summer |

| Target zone | 1.13 |

| Key risk | SoH reopening / softer US data |

The structure is attractive because it avoids paying for a full outright put while still monetizing a move toward the key downside zone.

## 1. US and Euro Area data trends are diverging

The first reason to short EUR/USD is the divergence in data momentum.

US data has continued to surprise to the upside relative to G10 peers. Markets are only starting to position for the risk that the Fed may need to keep policy tighter for longer, or even consider additional hikes if inflation and activity remain firm.

By contrast, ECB tightening expectations appear closer to reasonable limits. The Euro Area is facing more direct growth headwinds from higher energy prices, given its energy-import dependence and weaker terms of trade.

So the macro asymmetry is unfavorable for the euro:

- US data: resilient / upside surprises

- Euro Area data: more vulnerable to energy and growth drag

- Fed pricing: still room to reprice hawkishly

- ECB pricing: closer to limits

That creates a relative policy and growth backdrop that supports the dollar over the euro.

## 2. Rate differentials are moving against EUR/USD

EUR/USD has been slow to react to the renewed narrowing in Euro Area versus US forward rate differentials.

The key rate signal is that EA-US 1Y1Y differentials have moved against the euro. At the same time, the US 2Y versus Schatz 2Y spread appears to have bottomed and broken higher out of its prior channel.

That suggests further upside in US front-end yields relative to Germany, which should normally pressure EUR/USD lower.

The basic FX logic is straightforward:

- Higher relative US yields support USD.

- Lower relative Euro Area yields pressure EUR.

- If EUR/USD has lagged the move in rates, the FX adjustment may still be ahead.

This is one of the cleaner fundamental reasons to expect euro weakness.

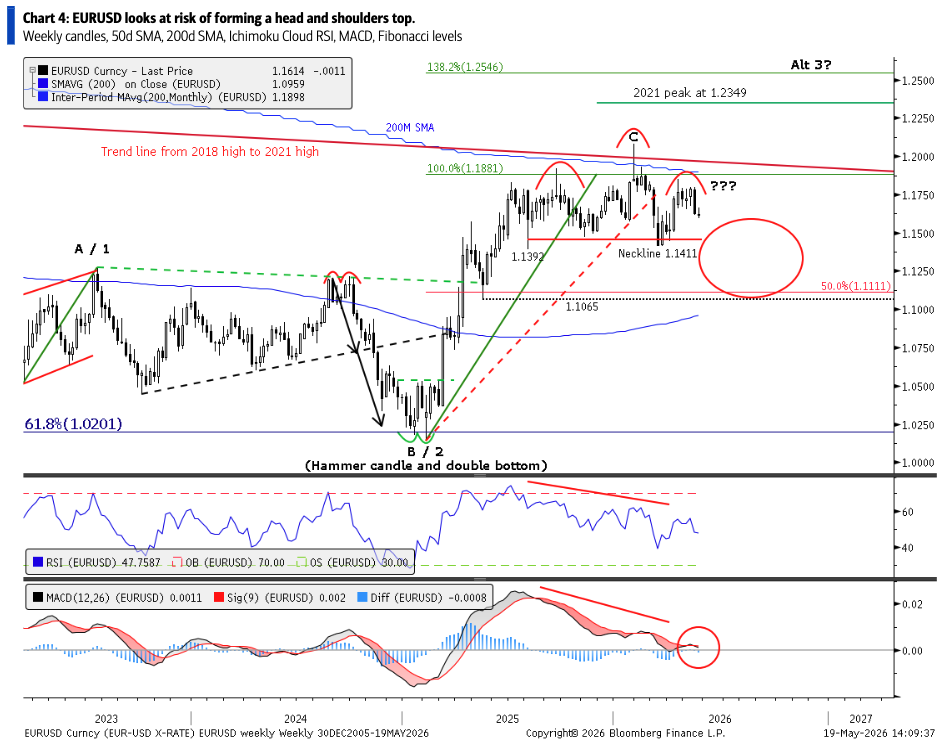

## 3. EUR/USD may be forming a head-and-shoulders top

Technically, EUR/USD may be forming a head-and-shoulders top.

The decline last week could represent the start of the right shoulder. A move down toward the neckline around 1.1411-1.1392 would increase conviction in the bearish pattern.

If EUR/USD breaks below that neckline, the downside potential opens toward 1.11 / 1.0950.

For now, the structure remains valid as long as EUR/USD stays below the resistance zone around 1.1797-1.1849.

Important levels:

| 1.1797-1.1849 | Pattern invalidation / resistance |

| 1.1411-1.1392 | Neckline |

| 1.13 | Put spread lower strike target |

| 1.11 / 1.0950 | Deeper measured downside |

The recommended put spread does not require a full breakdown to 1.10. It only needs a move toward 1.13 to monetize well.

## 4. DXY golden cross favors summer dollar strength

The DXY generated a golden cross signal on April 7, when the 50-day moving average crossed above the 200-day moving average.

Historically, after similar signals, DXY has tended to trade higher over the following 20-70 trading days around 65%-80% of the time. That window maps to roughly May through July, which supports the idea of summer USD strength.

This is a technical but historically supportive argument. It does not guarantee dollar upside, but it adds to the probability that DXY can remain firm over the next several months.

A stronger DXY typically means lower EUR/USD, given the euro’s large weight in the dollar index.

## 5. DXY is tracking the 2016-2018 Trump cycle

The current DXY path since President Trump’s November 2024 election has been tracking the pattern seen after his first election victory in November 2016.

In the 2016-2018 cycle, the DXY formed a bottom and then rallied sharply during the summer of 2018, gaining roughly 6.5%. EUR/USD declined over that period.

If the current pattern continues to rhyme, DXY could rally toward 103 / 104.70 this summer.

That would likely put material downside pressure on EUR/USD, especially if combined with rising US rate differentials and energy-driven Euro Area terms-of-trade stress.

## 6. Oil technicals favor upside, hurting the euro

Oil has consolidated over the past two months in a triangle pattern after bottoming and rallying earlier this year. In technical analysis, triangles often act as continuation patterns within existing trends.

If oil breaks higher, the next risk zone could be a rally into the USD 130s.

That would be negative for the euro because the Euro Area is a large energy importer. Higher oil worsens the region’s terms of trade, squeezes consumers and industry, and complicates ECB policy by raising inflation while weakening growth.

For EUR/USD, higher oil can therefore be bearish through several channels:

- Weaker Euro Area terms of trade

- Lower real income

- Growth drag

- Higher inflation volatility

- Less favorable risk sentiment

- Reduced room for ECB tightening relative to the Fed

This is especially relevant while the Strait of Hormuz remains a key macro risk.

## Why use a put spread rather than an outright short?

The put spread is useful because the bearish EUR/USD view is targeted but not unlimited.

A 1.15/1.13 put spread expresses the view that EUR/USD drifts lower into summer without requiring a collapse. It also limits premium cost and reduces exposure to adverse carry/vol dynamics.

Advantages:

- Lower premium than outright put

- Defined risk

- Monetizes move toward key support

- Good fit for moderate downside target

- Helps manage event risk around US-Iran headlines

The trade is not designed for a crash to parity. It is designed for a controlled move toward 1.13.

## Key risks to the trade

### 1. US-Iran deal and Strait reopening

The biggest risk is a credible US-Iran agreement that quickly reopens the Strait of Hormuz. That would likely push oil lower, ease Euro Area terms-of-trade pressure, reduce inflation fears, and improve risk sentiment.

This would support EUR/USD and hurt the put spread.

### 2. Summer seasonality

Summer seasonality can modestly support the euro. This is not the dominant driver, but it is a known headwind for a short EUR/USD position.

### 3. Softer US data

If US data softens, markets could price out Fed hike risk or reprice toward eventual cuts. That would weaken the dollar and support EUR/USD.

Given that the first reason for the trade is US data outperformance, any reversal in that trend would directly undermine the thesis.

### 4. ECB hawkish surprise

If the ECB pushes harder against inflation than expected, or if Euro Area data holds up better than feared, rate differentials could stop moving against the euro.

### 5. Failed technical breakdown

If EUR/USD holds above the neckline and then breaks above 1.1797-1.1849, the head-and-shoulders structure would lose validity.

## Trading takeaway

Short EUR/USD remains attractive into summer, but the best expression is a defined-risk put spread rather than an outright aggressive short.

The trade benefits from:

- Stronger US data

- Fed repricing risk

- Rate differentials moving against the euro

- Bearish EUR/USD technical setup

- DXY golden cross

- DXY tracking the 2016-2018 rally pattern

- Oil upside risk and Euro Area terms-of-trade pressure

The cleanest catalyst path is a combination of firm US data, sticky US yields, oil holding high or breaking higher, and EUR/USD losing the 1.1411-1.1392 neckline.

The recommended trade is to buy a 3-month EUR/USD 1.15/1.13 put spread for roughly 0.3591%, with spot at 1.1610.

The thesis is that EUR/USD is vulnerable into summer because US data and rate differentials are moving in favor of the dollar, technicals suggest a potential top, DXY momentum is improving, and oil upside would worsen the Euro Area terms-of-trade backdrop.

The main risks are a quick US-Iran deal that reopens the Strait, softer US data, and seasonal euro support. But as a defined-risk structure, the put spread offers a disciplined way to position for moderate euro weakness without overpaying for downside.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!